Fixing the Benefit “Notch” & Boosting Social Security During COVID

Rep. John Larson greets a constituent in Connecticut

The National Committee has endorsed a bill to avoid a significant drop in Social Security benefits for future retirees turning 60 this year. Rep. John Larson’s Social Security COVID-19 Correction and Equity Act repairs a glitch in current law which, if unchecked, would result in a sizable “notch” in retirement income for this age group.

Social Security benefits are calculated according to a formula that incorporates the average wage for the year that beneficiaries reach 60 years of age. Workers born in 1960 will have their benefits determined according to the average wage for 2020, which will be lower than usual due to the COVID crisis. The average beneficiary would take a $2,000 annual hit in their future Social Security benefits – and not just once, but for life.

“Rep. Larson’s bill would spare workers turning 60 this year from a painful and permanent benefit cut. Tomorrow’s retirees will depend even more on Social Security than the current generation of seniors. Americans should not be deprived tens of thousands of dollars in retirement income simply because they were born in the wrong year. The COVID-19 Correction and Equity Act offers a commonsense fix to an unintended consequence of Social Security law.” – Max Richtman, president and CEO of the National Committee to Preserve Social Security and Medicare

Larson’s bill corrects this problem – the result of flawed legislative language in the Social Security amendments of 1977 – by ensuring that the Average Wage Index (for Social Security’s purposes) never drops below the previous year’s level.

In addition to repairing the “notch,” Larson’s bill would make improvements to Social Security that would help ease the financial pain of the COVID crisis for retirees and people with disabilities, including millions of new claimants.

Here are some of the other major provisions in the Social Security COVID-19 Correction and Equity Act:

- Increases benefits by 2 percent;

- increases the threshold to 125 percent of the poverty level for the special minimum benefit, lifting more lifelong workers out of poverty;

- Reduces taxation on benefits for lower-middle income beneficiaries who are struggling to provide for themselves and their families.

“Certainly, the seniors who would lose massive amounts in Social Security benefits will thank Rep. Larson for finding a solution to the ‘notch.’ But the broad array of program improvements that have been included in the bill will benefit all Americans. We believe that they will prove to be especially helpful to women and those in communities of color who have been hardest hit by the COVID pandemic.” – Max Richtman

If Larson’s legislation passes the House, the bill as a whole may face headwinds in the Senate, where many pieces of legislation to help everyday America’s have perished in Leader McConnell’s “graveyard.” At the same time, the provision to fix the “notch” – an important technical correction more than a sweeping policy proposal – may survive. As Social Security champions in Congress continue to boost and strengthen the program during the COVID crisis and beyond, repairing the notch would spare those turning 60 this year an arbitrary and unnecessary benefit cut.

Read the National Committee’s endorsement letter of Rep. Larson’s bill here.

Independence for Seniors Requires Better Dental Coverage

With Independence Day close at hand, we’re reminded that good health is key to seniors remaining independent as they age. We have known for some time that good dental health, in particular, is fundamental to older Americans’ overall well-being. But a new survey by the Centers for Disease Control suggests that many seniors fall short of the mark in this area. Among other things, the survey shows that more than one in ten older Americans not only suffers from serious dental issues, but loses all of their teeth.

According to the National Health and Nutrition Examination Survey, roughly 13% of adults 65 and older suffer from complete tooth loss. For those 75 and older, the rate jumps to nearly 18%. Men, on average, had more severe tooth loss than women. The data also shows clear ethnic disparities, with 25% of non-Hispanic black seniors losing all of their teeth. These numbers are unacceptable in one of the wealthiest countries in the world.

Tooth loss and poor dental health in general can lead to problems with eating, speaking, and appearance – which can impede social interaction. Social interaction is a cornerstone of mental health for seniors. But tooth decay and loss also has been linked with serious medical conditions, including diabetes, hypertension, and cardiovascular disease.

The good news is: acute dental issues usually can be prevented with proper dental care. The bad news: two thirds of American seniors lack dental insurance. Patients without insurance are less likely to seek regular dental care. By the time they go to the dentist, their oral health may already be seriously compromised.

Unfortunately, traditional Medicare does not include routine dental coverage. Medicare beneficiaries must pay out of pocket for services such as oral exams, cleanings, fillings, bridges and crowns. The costs can easily run into the thousands of dollars. That’s unaffordable for many Medicare beneficiaries, whose average income is only $26,000 per year.

NON-HISPANIC BLACK SENIORS SUFFER TOOTH

LOSS SIGNIFICANTLY MORE THAN WHITES

Source: Centers for Disease Control

Routine dental care is not the only coverage that Medicare excludes. The program also does not cover routine vision or hearing care, even though problems with the eyes and ears can also lead to more serious medical issues. The National Committee to Preserve Social Security and Medicare has long advocated that Medicare be expanded to include all three – dental, vision, and hearing care, because it no longer makes sense to provide coverage for every part of seniors’ bodies except their eyes, ears, and teeth.

In fact, expanding Medicare to include these coverages could save the program money in the long run. Good dental, vision, and hearing care leads to better overall health outcomes – meaning fewer sicker seniors in the future. Medicare expansion is not a pie-in-the sky idea. In fact, the House of Representatives took a major step in this direction with the passage of H.R. 3, a landmark bill that would lower Medicare’s drug costs and use some of the savings for partial dental, vision, and hearing coverage.

A bill introduced by Rep. Lucille Roybal-Allard (D-CA) goes further. The Seniors Have Eyes, Ears, and Teeth Act would provide Medicare beneficiaries with comprehensive dental, vision, and hearing coverage. Meanwhile, Rep. Lloyd Doggett’s (D-TX) Medicare Dental, Vision, and Hearing Benefit Act would phase-in coverage over eight years, with some limitations.

Unfortunately, none of these bills is likely to be taken up by the Senate on Majority Leader Mitch McConnell’s watch. As one journalist put it, “There’s zero chance of that. Or less.” But if the 2020 elections result in a new President and new Senate majority, we would likely witness a Medicare expansion– including these crucial coverages. As with so many other issues affecting American seniors, their independence from serious dental, hearing and vision issues and the ensuing medical consequences – hinges on the outcome of November’s elections.

Workers Turning 60 This Year Face “Notch” in Benefits

Future Social Security beneficiaries turning 60 this year are in for a rude surprise: their monthly benefits may be lower than those born in previous years. Benefits for each age group are calculated based on the Average Wage Index (AWI) for the year they turn 60. Normally, average wages rise from year to year. But this year, because of the COVID pandemic, wages are likely to decrease by as much as 20%. Benefits for wage-earners in 2020 would then be as much as 15% lower than for workers hitting that milestone birthday in 2019. This incipient reduction is sometimes referred to as a “notch” in benefits for people born in 1960.

The notch for workers turning 60 this year is due to a glitch in Social Security law. Social Security benefits are based on the highest 35 years in a worker’s earning history. The Average Wage Index is applied to each year’s earnings in order to ensure that benefits are based on the dollar value of today’s wages vs. the year the wages were earned (which, for someone just turning 60, could date as far back as the late 1970s).

The AWI was introduced into the formula by the Social Security Amendments of 1977. The drafters of that legislation clearly did not anticipate that average wages would fall precipitously from one year to the other. In fact, since 1977, average wages have only declined one other time – at the height of the Great Recession in 2009. That dip was a relatively small 1.5% and “not big enough to catch people’s attention because the effects on benefits was negligible,” says Webster Phillips, NCPSSM’s chief Social Security expert.

Unfortunately, if no remedial action is taken, the benefit reduction for workers turning 60 in 2020 will be permanent. Their benefits will be lower than workers’ born before 1960 for life. Paul Van de Water of the Center on Budget and Policy Priorities provided a conservative estimate of the dollar-amount hit that this age cohort could take:

“If the average wage falls by (even) 5 percent in 2020… the retirement benefit of a 60-year-old worker with average earnings will drop by about $1,200 a year for each and every year of retirement.” – Paul Van de Water, Center on Budget and Policy Priorities

Of course, that worker’s annual cost-of-living adjustments (COLAs) would also be permanently reduced, causing further financial hardship. With 40% of seniors relying on for Social Security for all or most of their income – and many just skirting the edges of poverty on already modest benefits – a steep falloff in the AWI could cause retirees real financial distress.

“People shouldn’t suffer a large, permanent drop in their Social Security benefits just because they turn 60, become disabled, or experience the loss of a breadwinner around the start of a deep recession.” – Paul Van de Water, Center for Budget and Policy Priorities

In order to avoid unintentionally punishing people who turn 60 this year, Congress must take action before those workers begin claiming Social Security. (Sixty-two is the youngest age a worker can collect benefits; 67 is the Full Retirement Age for this age group.) Any change in Social Security law requires a 60-vote majority in the Senate.

Of course, the “notch” issue is only one of the challenges facing the program. Social Security will need a revenue boost in order to remain financially healthy for the remainder of this century. Retirees will need a benefit boost and a more accurate cost-of-living adjustment formula – simply to keep up with the increasing cost of essentials, from groceries to housing to health care. Seniors cannot afford benefit cuts – unintended or otherwise. Majorities in both Houses of Congress must summon the political will to increase revenues and benefits for the future. The best way to ensure that outcome is for voters to elect lawmakers in 2020 who are committed to just, equitable, and common-sense solutions that put the interests of American workers first.

Trump Administration No Friend to Seniors

President Trump at White House roundtable event, “Fighting for America’s Seniors”

With about five months until the 2020 elections, President Trump is underwater with senior voters – a demographic that he won in 2016. Since these polling numbers came out, the President has been making gestures toward older voters – one might say to curry favor – without advocating major policy changes that would significantly improve seniors’ lives. On Monday, President Trump held an event at the White House touting the administration’s supposed accomplishments in this area.

During this “Roundtable Discussion on Fighting for America’s Seniors,” the President touted an elder fraud hotline that the Dept. of Justice established this year, which has received some 1,800 calls. There is no doubt that criminals are preying on seniors using various scams around Social Security and Medicare – and that this activity has ratcheted up during the COVID pandemic. Any efforts to combat elder fraud are laudable.

Unfortunately, Trump used the elder fraud initiative as a springboard into some disingenuous claims about everything the administration has supposedly done for seniors. “We’re taking care of our senior citizens better than ever before,” he boasted. It’s an incredulous statement, not only in the wake of the pandemic that has claimed a disproportionate share of older Americans’ lives, but also in the broad sweep of history. Better than ever before? Better than FDR, who created Social Security? Better than LBJ, who signed Medicare and Medicaid into law? Better than President Obama, who provided older patients with protections from pre-existing conditions when seeking health insurance and made significant improvements to Medicare? The usual Trumpian hyperbole aside, the President made several claims about his administration’s ‘helpfulness’ to seniors during Monday’s event that don’t hold up.

TRUMP: “Last month, I announced the deal to slash out-of-pocket costs of insulin, and insulin is such a big deal and such a big factor of importance for our senior citizens. And we slashed costs for hundreds of thousands of Medicare beneficiaries.”

REALITY: The Trump administration announced that participating enhanced Medicare Part D prescription drug plans will allow beneficiaries to access insulin for a maximum copay of $35 for one month’s supply. Only patients who elect (and pay for) enhanced coverage will be able to take advantage of the $35 price cap – and only if their drug plans participate. Millions of seniors whose plans do not include this provision will continue to pay an average of over $1,100 in annual out of pocket insulin costs. The new policy does nothing to reduce the skyrocketing price of insulin.

TRUMP: “Average basic [Medicare] Part D [prescription drug] premiums have dropped 13.5 percent…”

Market forces, not the President, are mainly responsible for fluctuations in Medicare premiums. More importantly. premiums are not the only costs that seniors bear. Average out-of-pocket costs for Medicare beneficiaries have risen as premiums fluctuate. Many seniors, like other adults, choose plans with lower premiums without realizing that they may pay more out-of-pocket. At the end of 2018, US News and World Report indicated that, without federal intervention, “the prescription benefit in Medicare Part D will start drawing a lot more money out of the pockets of seniors taking pricey drugs.”

TRUMP: “As you know, last year was the first year where drug prices, in 52 years — where drug prices have actually gone down, the cost of prescription drugs.”

REALITY: The President likes to cite this statistic, but it is only one measure of drug prices and it is not the first time that this indicator has gone down in 52 years. This index reflects what the average consumer pays at retail pharmacies, not the actual costs of drugs. Meanwhile, prices for the most often-prescribed drugs for Medicare patients increased 10 times the rate of inflation during a recent five-year period. The popular anti-inflammatory, Humira – which seniors take for everything from arthritis to Crohn’s Disease – now costs up to $72,000 annually – with Medicare patients paying up to $5,000 out of pocket for this drug.

TRUMP: “We’re strongly defending Medicare and Social Security, and we always will.”

REALITY: This is probably the President’s most laughable claim regarding seniors. The Trump administration’s budgets have proposed cutting hundreds of billions of dollars from Medicare. The White House has relentlessly tried to repeal the Affordable Care Act, which made significant improvements to Medicare. The administration has proposed to cut Social Security Disability Insurance by tens of billions of dollars – and imposed a new rule to make it harder for people with disabilities to continue collecting benefits. The President has campaigned tirelessly to eliminate payroll taxes, which directly fund Social Security and Medicare, at a time when both programs need more, not less, revenue. The list goes on. This is the President’s notion of “strongly defending” both programs?

Meanwhile, seniors appear to strongly disagree with proposals from the White House and conservatives in Congress that would tamper with Social Security. This is made clear in a National Committee survey of its member and supporters released last week.

TRUMP: “We’ll always protect our senior citizens and everybody against preexisting conditions.”

REALITY: The opposite is true. The President has done everything to undermine protections for pre-existing conditions, especially for seniors. He tried to repeal the Affordable Care Act, which prevented health insurers from declining coverage for pre-existing conditions – which older patients tend to suffer from more than younger adults. The ACA also limited insurers’ ability to charge older patients higher premiums than younger ones. A president committed to protecting people with pre-existing conditions would not still be trying to destroy Obamacare. When the GOP-controlled Congress failed to repeal the ACA, the White House attempted to sabotage the program through administrative measures, and is still arguing (during a pandemic) that Obamacare should be struck down in the federal courts. The administration also began allowing junk insurance plans with high deductibles that do not protect patients with pre-existing conditions.

Instead of prevaricating and pandering, here is what the President would do if he were a true champion of seniors:

- Endorse legislation to expand and strengthen Social Security;

- Embrace the Lower Drug Costs Now Act, which would allow Medicare to negotiate prescription prices directly with Big Pharma;

- Stop promoting private Medicare Advantage plans over traditional Medicare;

- Significantly increase funding for the Social Security Administration to provide seniors with better customer service;

- Cease the campaign to eliminate Social Security and Medicare payroll taxes;

- Stop proposing $1.5 trillion in budget cuts to Medicare and Medicaid; Don’t propose to slash programs that help to feed lower income seniors and keep their homes heated in the winter;

- Condemn calls from conservatives to sacrifice seniors’ lives during COVID-19 for the sake of the economy.

These actions would go a long way toward “taking care of seniors,” but President Trump is not likely to take them. Perhaps that is why seniors, wary of this President’s commitment to their well-being – especially during the Coronavirus pandemic – have continued to turn away from him and may not vote Trump in 2020.

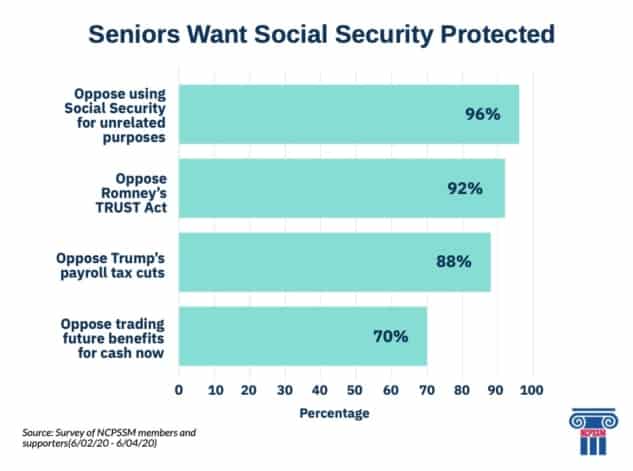

Survey Says: Seniors Want Social Security Protected, not Misused

A new survey of National Committee members and supporters suggests that the Trump administration and so-called “fiscal hawks” in Congress are seriously out of step with American seniors when it comes to Social Security. In the face of an intensifying campaign to undermine the program using the COVID pandemic as cover, the majority of respondents told us they want Social Security expanded – and not misused for unrelated purposes.

Ninety-six percent said they oppose the use of Social Security funds to pay for other fiscal priorities. In particular, 88% oppose President Trump’s reckless proposals to cut the payroll taxes that fund Social Security. These proposals would not only interfere with the program’s revenue stream, they would mostly benefit larger companies and higher earners, instead of the low-income workers who need the most financial relief during the pandemic.

Ninety-two percent of our members and supporters reject Senator Mitt Romney’s TRUST Act, which would establish “rescue committees” for Social Security’s trust funds – and would allow severe benefit cuts to be fast-tracked in Congress.

Seventy percent of respondents are against a new scheme (which White House aides considered) to give Americans the option of forfeiting some of their future Social Security benefits for emergency cash now.

The National committee recognizes that working Americans need relief from the financial pain of the COVID crisis. But we disagree that Social Security – a program funded by Americans workers – should be misappropriated for purposes having nothing to do with its core mission, which is to provide basic income upon retirement, disability, or the death of a family breadwinner. That is the very reason that President Franklin Roosevelt and his aides crafted Social Security as a worker-funded program – to protect it from politicians who might seek to misuse or dismantle it.

“This polling shows that many policymakers continue to be tone-deaf to the overwhelming support for social security and overwhelming opposition to proposals to tamper with Social Security. These proposals may be attractive to campaign donors on Wall Street, but certainly not among American seniors.” – Dan Adcock, Director of Government Relations and Policy, National Committee to Preserve Social Security and Medicare

While our members and supporters reject the President’s and fiscal hawks’ policies, they overwhelmingly support legislation to expand and strengthen Social Security. Ninety-two percent say it’s time to pass the Social Security 2100 Act, which would boost earned benefits and ensure Social Security’s long-term solvency.

The future of Social Security very much hinges on the outcome of the 2020 elections. If the President is re-elected and his party maintains its Senate majority, the harmful proposals that most Americans reject could take root. If, on the other hand, seniors vote in their own interests – as they did in 2018 – destructive policies can be blocked and legislation like the Social Security 2100 Act can be enacted, giving beneficiaries a much-needed raise and safeguarding the program’s financial future. Seniors need true champions in the White House and in Congress. The new poll results are an encouraging sign for seniors… and a stunning rebuke for Social Security’s opponents.

Fixing the Benefit “Notch” & Boosting Social Security During COVID

Rep. John Larson greets a constituent in Connecticut

The National Committee has endorsed a bill to avoid a significant drop in Social Security benefits for future retirees turning 60 this year. Rep. John Larson’s Social Security COVID-19 Correction and Equity Act repairs a glitch in current law which, if unchecked, would result in a sizable “notch” in retirement income for this age group.

Social Security benefits are calculated according to a formula that incorporates the average wage for the year that beneficiaries reach 60 years of age. Workers born in 1960 will have their benefits determined according to the average wage for 2020, which will be lower than usual due to the COVID crisis. The average beneficiary would take a $2,000 annual hit in their future Social Security benefits – and not just once, but for life.

“Rep. Larson’s bill would spare workers turning 60 this year from a painful and permanent benefit cut. Tomorrow’s retirees will depend even more on Social Security than the current generation of seniors. Americans should not be deprived tens of thousands of dollars in retirement income simply because they were born in the wrong year. The COVID-19 Correction and Equity Act offers a commonsense fix to an unintended consequence of Social Security law.” – Max Richtman, president and CEO of the National Committee to Preserve Social Security and Medicare

Larson’s bill corrects this problem – the result of flawed legislative language in the Social Security amendments of 1977 – by ensuring that the Average Wage Index (for Social Security’s purposes) never drops below the previous year’s level.

In addition to repairing the “notch,” Larson’s bill would make improvements to Social Security that would help ease the financial pain of the COVID crisis for retirees and people with disabilities, including millions of new claimants.

Here are some of the other major provisions in the Social Security COVID-19 Correction and Equity Act:

- Increases benefits by 2 percent;

- increases the threshold to 125 percent of the poverty level for the special minimum benefit, lifting more lifelong workers out of poverty;

- Reduces taxation on benefits for lower-middle income beneficiaries who are struggling to provide for themselves and their families.

“Certainly, the seniors who would lose massive amounts in Social Security benefits will thank Rep. Larson for finding a solution to the ‘notch.’ But the broad array of program improvements that have been included in the bill will benefit all Americans. We believe that they will prove to be especially helpful to women and those in communities of color who have been hardest hit by the COVID pandemic.” – Max Richtman

If Larson’s legislation passes the House, the bill as a whole may face headwinds in the Senate, where many pieces of legislation to help everyday America’s have perished in Leader McConnell’s “graveyard.” At the same time, the provision to fix the “notch” – an important technical correction more than a sweeping policy proposal – may survive. As Social Security champions in Congress continue to boost and strengthen the program during the COVID crisis and beyond, repairing the notch would spare those turning 60 this year an arbitrary and unnecessary benefit cut.

Read the National Committee’s endorsement letter of Rep. Larson’s bill here.

Independence for Seniors Requires Better Dental Coverage

With Independence Day close at hand, we’re reminded that good health is key to seniors remaining independent as they age. We have known for some time that good dental health, in particular, is fundamental to older Americans’ overall well-being. But a new survey by the Centers for Disease Control suggests that many seniors fall short of the mark in this area. Among other things, the survey shows that more than one in ten older Americans not only suffers from serious dental issues, but loses all of their teeth.

According to the National Health and Nutrition Examination Survey, roughly 13% of adults 65 and older suffer from complete tooth loss. For those 75 and older, the rate jumps to nearly 18%. Men, on average, had more severe tooth loss than women. The data also shows clear ethnic disparities, with 25% of non-Hispanic black seniors losing all of their teeth. These numbers are unacceptable in one of the wealthiest countries in the world.

Tooth loss and poor dental health in general can lead to problems with eating, speaking, and appearance – which can impede social interaction. Social interaction is a cornerstone of mental health for seniors. But tooth decay and loss also has been linked with serious medical conditions, including diabetes, hypertension, and cardiovascular disease.

The good news is: acute dental issues usually can be prevented with proper dental care. The bad news: two thirds of American seniors lack dental insurance. Patients without insurance are less likely to seek regular dental care. By the time they go to the dentist, their oral health may already be seriously compromised.

Unfortunately, traditional Medicare does not include routine dental coverage. Medicare beneficiaries must pay out of pocket for services such as oral exams, cleanings, fillings, bridges and crowns. The costs can easily run into the thousands of dollars. That’s unaffordable for many Medicare beneficiaries, whose average income is only $26,000 per year.

NON-HISPANIC BLACK SENIORS SUFFER TOOTH

LOSS SIGNIFICANTLY MORE THAN WHITES

Source: Centers for Disease Control

Routine dental care is not the only coverage that Medicare excludes. The program also does not cover routine vision or hearing care, even though problems with the eyes and ears can also lead to more serious medical issues. The National Committee to Preserve Social Security and Medicare has long advocated that Medicare be expanded to include all three – dental, vision, and hearing care, because it no longer makes sense to provide coverage for every part of seniors’ bodies except their eyes, ears, and teeth.

In fact, expanding Medicare to include these coverages could save the program money in the long run. Good dental, vision, and hearing care leads to better overall health outcomes – meaning fewer sicker seniors in the future. Medicare expansion is not a pie-in-the sky idea. In fact, the House of Representatives took a major step in this direction with the passage of H.R. 3, a landmark bill that would lower Medicare’s drug costs and use some of the savings for partial dental, vision, and hearing coverage.

A bill introduced by Rep. Lucille Roybal-Allard (D-CA) goes further. The Seniors Have Eyes, Ears, and Teeth Act would provide Medicare beneficiaries with comprehensive dental, vision, and hearing coverage. Meanwhile, Rep. Lloyd Doggett’s (D-TX) Medicare Dental, Vision, and Hearing Benefit Act would phase-in coverage over eight years, with some limitations.

Unfortunately, none of these bills is likely to be taken up by the Senate on Majority Leader Mitch McConnell’s watch. As one journalist put it, “There’s zero chance of that. Or less.” But if the 2020 elections result in a new President and new Senate majority, we would likely witness a Medicare expansion– including these crucial coverages. As with so many other issues affecting American seniors, their independence from serious dental, hearing and vision issues and the ensuing medical consequences – hinges on the outcome of November’s elections.

Workers Turning 60 This Year Face “Notch” in Benefits

Future Social Security beneficiaries turning 60 this year are in for a rude surprise: their monthly benefits may be lower than those born in previous years. Benefits for each age group are calculated based on the Average Wage Index (AWI) for the year they turn 60. Normally, average wages rise from year to year. But this year, because of the COVID pandemic, wages are likely to decrease by as much as 20%. Benefits for wage-earners in 2020 would then be as much as 15% lower than for workers hitting that milestone birthday in 2019. This incipient reduction is sometimes referred to as a “notch” in benefits for people born in 1960.

The notch for workers turning 60 this year is due to a glitch in Social Security law. Social Security benefits are based on the highest 35 years in a worker’s earning history. The Average Wage Index is applied to each year’s earnings in order to ensure that benefits are based on the dollar value of today’s wages vs. the year the wages were earned (which, for someone just turning 60, could date as far back as the late 1970s).

The AWI was introduced into the formula by the Social Security Amendments of 1977. The drafters of that legislation clearly did not anticipate that average wages would fall precipitously from one year to the other. In fact, since 1977, average wages have only declined one other time – at the height of the Great Recession in 2009. That dip was a relatively small 1.5% and “not big enough to catch people’s attention because the effects on benefits was negligible,” says Webster Phillips, NCPSSM’s chief Social Security expert.

Unfortunately, if no remedial action is taken, the benefit reduction for workers turning 60 in 2020 will be permanent. Their benefits will be lower than workers’ born before 1960 for life. Paul Van de Water of the Center on Budget and Policy Priorities provided a conservative estimate of the dollar-amount hit that this age cohort could take:

“If the average wage falls by (even) 5 percent in 2020… the retirement benefit of a 60-year-old worker with average earnings will drop by about $1,200 a year for each and every year of retirement.” – Paul Van de Water, Center on Budget and Policy Priorities

Of course, that worker’s annual cost-of-living adjustments (COLAs) would also be permanently reduced, causing further financial hardship. With 40% of seniors relying on for Social Security for all or most of their income – and many just skirting the edges of poverty on already modest benefits – a steep falloff in the AWI could cause retirees real financial distress.

“People shouldn’t suffer a large, permanent drop in their Social Security benefits just because they turn 60, become disabled, or experience the loss of a breadwinner around the start of a deep recession.” – Paul Van de Water, Center for Budget and Policy Priorities

In order to avoid unintentionally punishing people who turn 60 this year, Congress must take action before those workers begin claiming Social Security. (Sixty-two is the youngest age a worker can collect benefits; 67 is the Full Retirement Age for this age group.) Any change in Social Security law requires a 60-vote majority in the Senate.

Of course, the “notch” issue is only one of the challenges facing the program. Social Security will need a revenue boost in order to remain financially healthy for the remainder of this century. Retirees will need a benefit boost and a more accurate cost-of-living adjustment formula – simply to keep up with the increasing cost of essentials, from groceries to housing to health care. Seniors cannot afford benefit cuts – unintended or otherwise. Majorities in both Houses of Congress must summon the political will to increase revenues and benefits for the future. The best way to ensure that outcome is for voters to elect lawmakers in 2020 who are committed to just, equitable, and common-sense solutions that put the interests of American workers first.

Trump Administration No Friend to Seniors

President Trump at White House roundtable event, “Fighting for America’s Seniors”

With about five months until the 2020 elections, President Trump is underwater with senior voters – a demographic that he won in 2016. Since these polling numbers came out, the President has been making gestures toward older voters – one might say to curry favor – without advocating major policy changes that would significantly improve seniors’ lives. On Monday, President Trump held an event at the White House touting the administration’s supposed accomplishments in this area.

During this “Roundtable Discussion on Fighting for America’s Seniors,” the President touted an elder fraud hotline that the Dept. of Justice established this year, which has received some 1,800 calls. There is no doubt that criminals are preying on seniors using various scams around Social Security and Medicare – and that this activity has ratcheted up during the COVID pandemic. Any efforts to combat elder fraud are laudable.

Unfortunately, Trump used the elder fraud initiative as a springboard into some disingenuous claims about everything the administration has supposedly done for seniors. “We’re taking care of our senior citizens better than ever before,” he boasted. It’s an incredulous statement, not only in the wake of the pandemic that has claimed a disproportionate share of older Americans’ lives, but also in the broad sweep of history. Better than ever before? Better than FDR, who created Social Security? Better than LBJ, who signed Medicare and Medicaid into law? Better than President Obama, who provided older patients with protections from pre-existing conditions when seeking health insurance and made significant improvements to Medicare? The usual Trumpian hyperbole aside, the President made several claims about his administration’s ‘helpfulness’ to seniors during Monday’s event that don’t hold up.

TRUMP: “Last month, I announced the deal to slash out-of-pocket costs of insulin, and insulin is such a big deal and such a big factor of importance for our senior citizens. And we slashed costs for hundreds of thousands of Medicare beneficiaries.”

REALITY: The Trump administration announced that participating enhanced Medicare Part D prescription drug plans will allow beneficiaries to access insulin for a maximum copay of $35 for one month’s supply. Only patients who elect (and pay for) enhanced coverage will be able to take advantage of the $35 price cap – and only if their drug plans participate. Millions of seniors whose plans do not include this provision will continue to pay an average of over $1,100 in annual out of pocket insulin costs. The new policy does nothing to reduce the skyrocketing price of insulin.

TRUMP: “Average basic [Medicare] Part D [prescription drug] premiums have dropped 13.5 percent…”

Market forces, not the President, are mainly responsible for fluctuations in Medicare premiums. More importantly. premiums are not the only costs that seniors bear. Average out-of-pocket costs for Medicare beneficiaries have risen as premiums fluctuate. Many seniors, like other adults, choose plans with lower premiums without realizing that they may pay more out-of-pocket. At the end of 2018, US News and World Report indicated that, without federal intervention, “the prescription benefit in Medicare Part D will start drawing a lot more money out of the pockets of seniors taking pricey drugs.”

TRUMP: “As you know, last year was the first year where drug prices, in 52 years — where drug prices have actually gone down, the cost of prescription drugs.”

REALITY: The President likes to cite this statistic, but it is only one measure of drug prices and it is not the first time that this indicator has gone down in 52 years. This index reflects what the average consumer pays at retail pharmacies, not the actual costs of drugs. Meanwhile, prices for the most often-prescribed drugs for Medicare patients increased 10 times the rate of inflation during a recent five-year period. The popular anti-inflammatory, Humira – which seniors take for everything from arthritis to Crohn’s Disease – now costs up to $72,000 annually – with Medicare patients paying up to $5,000 out of pocket for this drug.

TRUMP: “We’re strongly defending Medicare and Social Security, and we always will.”

REALITY: This is probably the President’s most laughable claim regarding seniors. The Trump administration’s budgets have proposed cutting hundreds of billions of dollars from Medicare. The White House has relentlessly tried to repeal the Affordable Care Act, which made significant improvements to Medicare. The administration has proposed to cut Social Security Disability Insurance by tens of billions of dollars – and imposed a new rule to make it harder for people with disabilities to continue collecting benefits. The President has campaigned tirelessly to eliminate payroll taxes, which directly fund Social Security and Medicare, at a time when both programs need more, not less, revenue. The list goes on. This is the President’s notion of “strongly defending” both programs?

Meanwhile, seniors appear to strongly disagree with proposals from the White House and conservatives in Congress that would tamper with Social Security. This is made clear in a National Committee survey of its member and supporters released last week.

TRUMP: “We’ll always protect our senior citizens and everybody against preexisting conditions.”

REALITY: The opposite is true. The President has done everything to undermine protections for pre-existing conditions, especially for seniors. He tried to repeal the Affordable Care Act, which prevented health insurers from declining coverage for pre-existing conditions – which older patients tend to suffer from more than younger adults. The ACA also limited insurers’ ability to charge older patients higher premiums than younger ones. A president committed to protecting people with pre-existing conditions would not still be trying to destroy Obamacare. When the GOP-controlled Congress failed to repeal the ACA, the White House attempted to sabotage the program through administrative measures, and is still arguing (during a pandemic) that Obamacare should be struck down in the federal courts. The administration also began allowing junk insurance plans with high deductibles that do not protect patients with pre-existing conditions.

Instead of prevaricating and pandering, here is what the President would do if he were a true champion of seniors:

- Endorse legislation to expand and strengthen Social Security;

- Embrace the Lower Drug Costs Now Act, which would allow Medicare to negotiate prescription prices directly with Big Pharma;

- Stop promoting private Medicare Advantage plans over traditional Medicare;

- Significantly increase funding for the Social Security Administration to provide seniors with better customer service;

- Cease the campaign to eliminate Social Security and Medicare payroll taxes;

- Stop proposing $1.5 trillion in budget cuts to Medicare and Medicaid; Don’t propose to slash programs that help to feed lower income seniors and keep their homes heated in the winter;

- Condemn calls from conservatives to sacrifice seniors’ lives during COVID-19 for the sake of the economy.

These actions would go a long way toward “taking care of seniors,” but President Trump is not likely to take them. Perhaps that is why seniors, wary of this President’s commitment to their well-being – especially during the Coronavirus pandemic – have continued to turn away from him and may not vote Trump in 2020.

Survey Says: Seniors Want Social Security Protected, not Misused

A new survey of National Committee members and supporters suggests that the Trump administration and so-called “fiscal hawks” in Congress are seriously out of step with American seniors when it comes to Social Security. In the face of an intensifying campaign to undermine the program using the COVID pandemic as cover, the majority of respondents told us they want Social Security expanded – and not misused for unrelated purposes.

Ninety-six percent said they oppose the use of Social Security funds to pay for other fiscal priorities. In particular, 88% oppose President Trump’s reckless proposals to cut the payroll taxes that fund Social Security. These proposals would not only interfere with the program’s revenue stream, they would mostly benefit larger companies and higher earners, instead of the low-income workers who need the most financial relief during the pandemic.

Ninety-two percent of our members and supporters reject Senator Mitt Romney’s TRUST Act, which would establish “rescue committees” for Social Security’s trust funds – and would allow severe benefit cuts to be fast-tracked in Congress.

Seventy percent of respondents are against a new scheme (which White House aides considered) to give Americans the option of forfeiting some of their future Social Security benefits for emergency cash now.

The National committee recognizes that working Americans need relief from the financial pain of the COVID crisis. But we disagree that Social Security – a program funded by Americans workers – should be misappropriated for purposes having nothing to do with its core mission, which is to provide basic income upon retirement, disability, or the death of a family breadwinner. That is the very reason that President Franklin Roosevelt and his aides crafted Social Security as a worker-funded program – to protect it from politicians who might seek to misuse or dismantle it.

“This polling shows that many policymakers continue to be tone-deaf to the overwhelming support for social security and overwhelming opposition to proposals to tamper with Social Security. These proposals may be attractive to campaign donors on Wall Street, but certainly not among American seniors.” – Dan Adcock, Director of Government Relations and Policy, National Committee to Preserve Social Security and Medicare

While our members and supporters reject the President’s and fiscal hawks’ policies, they overwhelmingly support legislation to expand and strengthen Social Security. Ninety-two percent say it’s time to pass the Social Security 2100 Act, which would boost earned benefits and ensure Social Security’s long-term solvency.

The future of Social Security very much hinges on the outcome of the 2020 elections. If the President is re-elected and his party maintains its Senate majority, the harmful proposals that most Americans reject could take root. If, on the other hand, seniors vote in their own interests – as they did in 2018 – destructive policies can be blocked and legislation like the Social Security 2100 Act can be enacted, giving beneficiaries a much-needed raise and safeguarding the program’s financial future. Seniors need true champions in the White House and in Congress. The new poll results are an encouraging sign for seniors… and a stunning rebuke for Social Security’s opponents.